Is Xbox Game Pass Burning Money?

Share the Story:

Update to Article:- As of October 2025, Xbox have increased the cost of Xbox Game Pass again, adding $10/£8 respectivly to the Ulitmate tier now $29.99/£22.99. And the PC Game Pass tier rose from £9.99/$11.99 to £13.50/$16.50 for your rental based gaming fix. I think this is counter productive from the team. As it will cause a mass exodus of subscribers from the service and in the short and long term, will just make Game Pass even less attractive and more expensive for the team. Watch this space but I expect the market will cause them to rethink this change at a later date. Maybe with a new mid tier, reduction of big games such as Call of Duty from the service, or even a price reduction. Worse still would be all three, only time and the tide will tell.

Xbox repeats history again

As Microsoft have now officially come clean on what I had been discussing for years, their Multi-Platform publishing aims. Following the latest Xbox Developer direct they closed the final gap in that plan, console exclusivity. We learnt the brand new Fable title from Playground games will be day and date on PS5 alongside PC and Xbox Series consoles. Xbox have followed in SEGA’s path ever since they entered the console arena shortly after SEGA’s exit. And now, again, they have followed them into the mutli-platform software publisher. Following on from my Gaming bubble burst video 2 years ago now, I wanted to cover some real numbers on why this slow death of Xbox, as we knew them, happened and what I, and many others warned was the only future they had.

Is this... https://t.co/riye1mI5WU pic.twitter.com/5Og6Ku0jRa

— Michael T (@N_X_G) February 12, 2024

It's all part of the plan... https://t.co/mM2icWDUnU pic.twitter.com/1sfWyv7T96

— Michael T (@N_X_G) July 10, 2024

They made no money on Gamepass(GP), undoubtly the biggest shadow across the industry over the past 5 years. The ongoing battle of is GP profitable or not, seems to flip flop on both sides of the fence. On one side, The haters will hate and know “without doubt in their hearts” it makes no money! On the other, are those that still hope for an Xbox days of yonder, “Know” it does make money, as it say’s so in the tea leaves. As I often say, there are lies, damn lies and statistics (well Tom Sawyer said it first) but I often extend with accountants. Within my own industry role I call them the 100% club, ‘Them‘ being sales and finance. They always manage to turn a negative into a positive and with Microsoft’s qtr earnings, like MANY public companies’ mind, they often change metrics to suit, changing measurements or stop reporting entirely on things if they do not align to their aims or results any longer, see sales of games vs user engagement.

Tell me lies, tell me sweet little lies

Take GAAP (General Accepted Accounting Practice) most companies that deal in international markets change certain reporting to reflect local and foreign currency changes. Which stop huge swings in market rates shifting qtr to qtr comparisons, these are normally reflected by reporting as is, but it is often done with a NON-GAAP measure which can be calculated many ways and these are ALWAYS done to present the best balance sheet. For example:- if last qtr the £ or $ dropped 15% against the euro or yen, then I may report a loss or gain from sales in each region in my overall rate. If that was a gain, I would likely report GAAP and look great (and accurate), but if I decided my biggest external market was costing me 15% off the top of my earnings, I might wince at that on paper. So, I can take last qtr exchange rate, where it looks better, report that and add an * for those that care. OR I could average out the past year as whole if that works even better, and again NON GAAP * and I am good. Now this is minor and often done, but it presents a small sample of what Common accountancy practises are. With Gamepass, I have said before, it is a Profit centre or a Cost centre, which ever best suits the accountant. And what this means is within Xbox and Microsoft, they can split out the OPcost, from revenue. The cost of sale from the profit margin, marketing, service and infrastructure. I do not know the specifics but they do this as they confirmed they DO NOT factor in 1st party games Loss of Sales OR Development into Gamepass figures. Now Here is where the ? from the online discourse stems from, helped in no small part by Chris Ding being ‘inconsistent‘ at best, but muddled with what he has reported.

The reality is, an accountant will always report what looks best, will always use the tools within their vast arsenal to improve this, and where possible they will often massage all areas of a business finance to best balance revenue, cash flow, and profit. Why do you think so many companies support charities for example, or Green renewable plans, it is most often not for the good in their heart. Now the quarterly results tell us a great deal, like cash flow reducing, big losses on Microsoft’s investment(s) in OPENAI, both in the $30 billion sunk cost, but also the share drop and the fact the bubble that AI exists within, may already be stretched to bursting. Not just for Microsoft but Google, Anthropic, Amazon, and even Nvidia. In short, the Big M have gotten into Bed with AI as the future and this is driving their core business, investment in land, bricks, tin and power from datacentres and such to expand into it. The issue is they are chasing the market here by a field yard or more and the reason I say this, is because this is driving much of the cutbacks and layoffs. From the commercial, corperate and gaming divisions as the billions in acquisitions can no longer be subsidised by other parts of Microsoft, namely Cloud, SaaS, Azure, 365, etc. And Game Pass is part of that equation and as a 3rd party publisher, the single biggest now, the latest cuts appear as if, IMHOP, Nadella is saying to Phil and co,

You can clean your own room from now on!

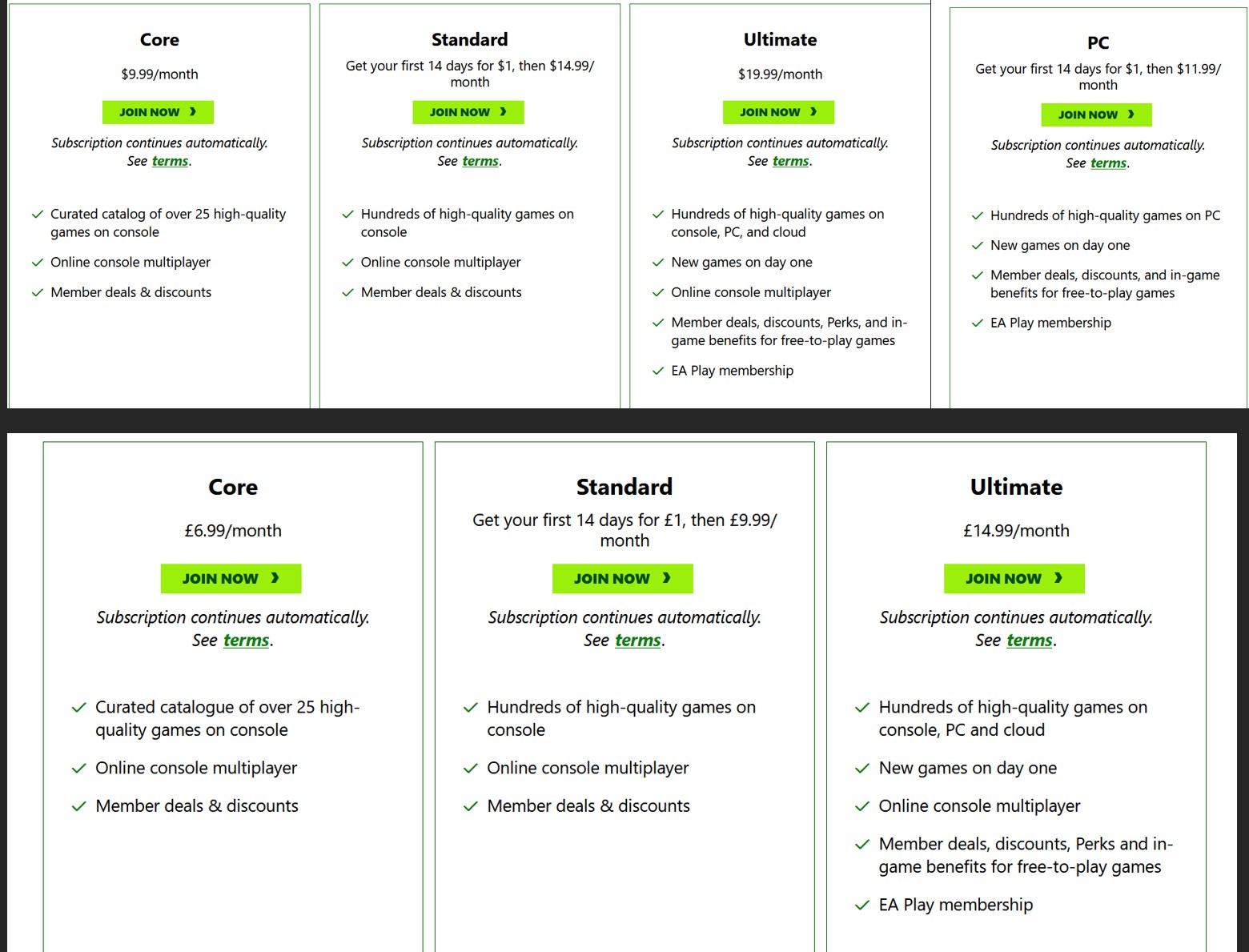

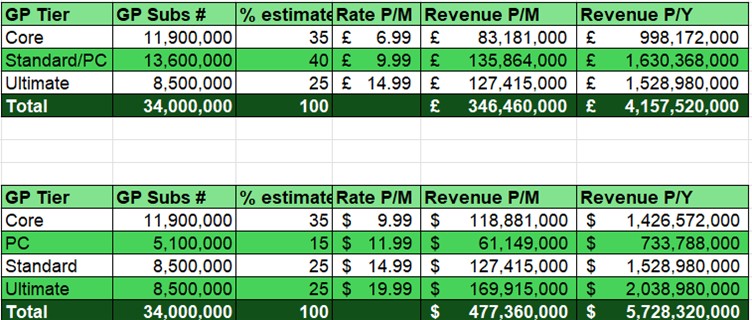

So, using that little example, which we know is true, lets take a look at the books from Microsoft themselves and see what we can work out as an example of how bad that impact may be. I stress I know accounting to a level within my job, mostly bids, BAFOs, ROMs, etc to full multi-year fixed price, T&M, Best Endeavours, SI, Sub-contract, services for support and other such commercial delivery mechanisms that cover a great deal of these areas. But I am NOT an accountant and do not profess to be, but I know enough to talk about it with some level of certainty. For this example, and based on what I think has happened within Microsoft and Xbox, we will assume that EVERYTHING is funded by Xbox themselves. From staff, marketing, development, power, tea & coffee, the whole shebang. The last Official figure from Xbox themselves on Game Pass subs was from Sarah Bond back in 2024 with 34 million BUT, this was also when Microsoft merged Xbox Live into Game Pass light. Surmising that at least 5-8 million (maybe more) of those came from Xbox Live becoming Game Pass core, so £6.99pm which DOES NOT include Day 1 1st party games or even the full catalogue, instead a curated 25 games of High quality. The next tier, Standard, also DOES NOT include day1 games but at least the full catalogue of games can be played (after a period of locked retail has passed mind). No, only the top tier, £14.99pm, Ultimate covers day one 1st party and discounts. Now, this figure only rose by 9 Million in just over 2 years, so the assumption again on my behalf. 8 Million of those were Xbox Live Gold, now core, and 1 million were brand new subscribers aka true growth. These subscriptions and potential distrubution of them breaks down as below:-

Playing with Numbers

GamePass is bringing in $477m per month revenue for Xbox, which equates to just under $5.8billion P/Year. Estimated, and may swing up or down +/- a billion a year, very likely, due to month-to-month changes of userbase, i.e. when a big new game lands, but enough for estimates. All these users need to connect and play from somewhere, and contrary to the marketing myth, the Cloud is not a place, it is a metaphor for Data Centres (DCs). As of the date of this Article, July 25, Microsoft has approx 400 DC across the globe in over 40 regions. Of which let’s assume a mixed ‘total’ of 14 support Game pass and Xcloud ( a part of Gamepass Ultimate) and recall Game Pass is only available in 27 countries, more countries cannot get the full cloud option than can. Infrastructure is the reason, and why from Microsoft to Sony and even Amazon, all stagger and roll-out in phases due to that cost. Microsoft alone spent $20 billion this year (2025) on this which is needed for that Ai drive alone, but back to gaming. Being generous we will assume that Xbox only has to pay for Two of these from scratch in the past year, but assume at least that figure + 50% year on year if they plan to achieve the 110 million GP users by 2030, likely more. From my Experience in working with and on DCs for years, Two things are always true: –

– Estimated costs are always wrong, about 40-85% higher than at start,

– Op costs are also always higher, and rarely go anywhere but up.

That said, we need a number, so let’s use my figures based on recent projects I have delivered as a guide (stress not exact) and we will ignore land purchase, local planning, legal etc for this which is potentially 100s of millions on its own. We are hovering well into estimates here and this would need to be factored up and down depending on region, but if we take these UK costs and convert to Dollars we are over $1.1 billion of that revenue gone just to keep the lights on in the DCs. But this is nothing, lets again assume incorrectly, that all Microsoft/XBOX current infrastructure is factored within the entire Xbox Studios operating income from 1st party and 3rd party sales for support. Be they websites, helpdesk, returns, R&D, HR, Accounting, etc. But that DOES NOT and SHOULD NOT include the cost of 3rd party deals into Game Pass OR the lost revenue on full price games, and at least a percentage of Op and Dev cost from any 1st party title that is sold into Game Pass, no, that should all be funded by Gamepass.

1st Party, 2nd Tier

In the last year or so we have had a bumper 1st party year from Xbox, and in that time we have seen some big hitter’s land. Taking figures made public in Indiana Jones and the Great Circl, Doom: The Dark Ages, and Oblivion Remastered. We know that Oblivion was the only one in the black from a development to profit perspective and remasters are very, very cheap compared to new games. But this only takes into account the sales from NON Game Pass markets, of which Xbox themselves are so small as to not be relevant. Effectively if they were 1st party only on Xbox it is simply not sustainable due to the cannibalising it has had on their own customers mindset and thus market. Quite simply causing the slow and steady death of the Xbox brand, almost exclusively, by Xbox’s own hands via poor strategy and management, not understanding their own market and audience and, ultimately, blindly following the “Netflix is the future” mantra. And this is what has led us to the current position myself and others warned off all those years ago, Activision was simply the final nail in that coffin.

Taking the latest mix of 1st party games, even with all external sales taken into account, estimates remember. Then they loose money on all games bar Oblivion, but if we took Xbox game pass on its sold, self supporting, origins, to the open market and stakeholders. It does not come close to washing its feet, let alone its face. This mix of 1st party then 3rd party game that did ok on gamepass but MUCH better on other platforms for both the publisher AND the platform holder, Xbox are almost $150 million in the red, without Oblivion it would be closer to double that, and this is just 6 games. Across an average of 4.5 year dev time. And NOW you see why they cut so many projects and teams, as the sunk cost was not worth chasing back, as most of those would also be loss leaders for Xbox Studios from the get go. Lets assume that they have 20 games in active development at any given year across all their studios and a further 10 big titles from 3rd party deals each year. We extrapolate these 6 games into 30 and average the dev and sales cost as a figure across four qtrs and we hit almost $4 billion on that cost alone, which does not cover the entire Dev cost of each studio, legal, location, equipment etc or even the vast cost of every 3rd party game cost from the those same subs. But for now, close enough to give you a view, add in that Infrastructure run rate for Game Pass/ Xcloud itself and that figure balloons to nigh on $5.5 Billion per year, and that potential $ 4.2 billion revenue stream being profitable is gone.

Game Pass is NOT the future

Now likelihood these are not the real figures, likelihood is they are better/worse for each, but the net result is likely the same. Game Pass and Xbox as a platform losses money, month on month, year on year and even with current sales factored in, that remains true. The 3rd party acquisitions have done nothing to solve that, on their own, but what they have done and were purchased for, was to create a growth stream of revenue to plug the leaking boat. The only way it was ever going to go, open up ALL games to PC, then PS5, then Nintendo and slowly chip away the Xbox fascade to reveal the Blue Sega within. We have now completed that journey and with recent releases on PS5 such as Forza and Microsoft Flight Simulator, selling millions more that on Xbox within months of release demonstrates the writing on my wall many moons ago. Game Pass is another revenue stream that is helping to subsidise the publisher arm of Xbox and the partnerships with Asus in the ROG Ally X, the upcoming Xbox next gen console that will be a PC in all but name, able to load Steam, Windows and even Office products most likely. This all now points to the fact Xbox, as we all knew it, is now dead and indeed it died almost 5 years ago to the day when Game Pass became the path they chose. The only thing left to see, is how successful they can make their new publishing future.